High-Yield Savings vs. CDs in 2026: Where to Park Your Cash for Maximum Returns

Published: March 8, 2026 | Last Updated: March 8, 2026

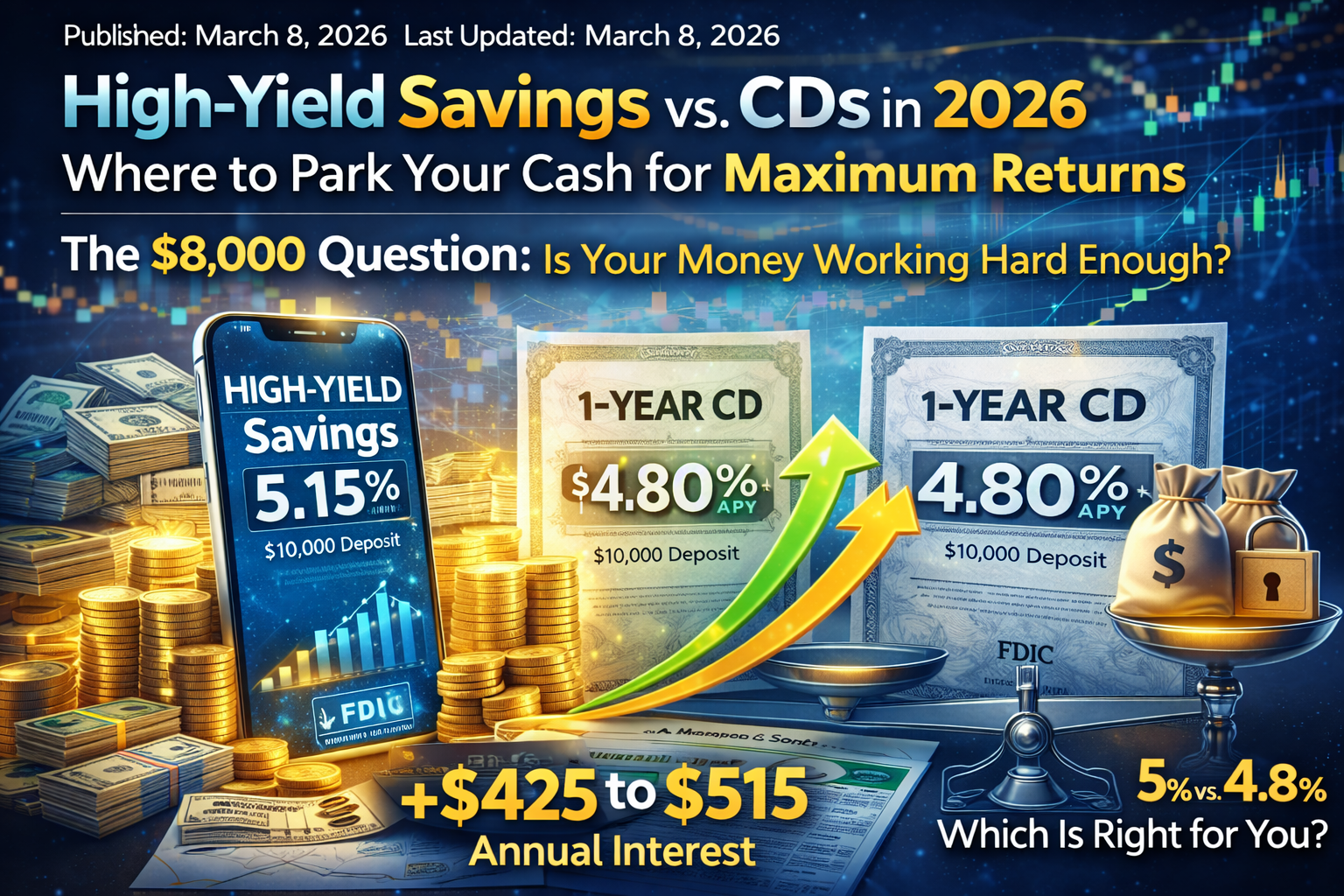

The $8,000 Question: Is Your Money Working Hard Enough?

If you have $10,000 sitting in a traditional savings account earning 0.46% APY—the national average as of early 2026—you’re leaving $800+ in annual interest on the table.

Right now, top high-yield savings accounts (HYSAs) pay 4.25%–5.15% APY. On that same $10,000, that’s $425–$515 per year in passive income. Risk-free. FDIC-insured. No lock-up period.

But 2026 brings a twist: Certificate of Deposit (CD) rates have inverted. Some 1-year CDs now pay less than HYSAs, breaking the traditional “longer term = higher rate” rule. Meanwhile, the Federal Reserve’s pause on rate cuts has created a window where savvy savers can lock in 5%+ returns—but for how long?

This guide breaks down exactly where to park your cash in 2026, whether HYSAs or CDs win for your goals, and the traps that eat into your returns.

Disclosure: This article contains affiliate links. We may receive compensation if you open an account through our links, at no cost to you. All opinions are our own. Rates and terms are subject to change. See our full advertiser disclosure at the bottom of this page.

Part 1: The 2026 Rate Landscape—What’s Actually Available

Current Rates (March 2026)

| Account Type | Top APY | Average APY | Minimum Deposit |

|---|---|---|---|

| Traditional Savings | 0.46% | 0.42% | $0 |

| High-Yield Savings | 5.15% | 4.35% | $0–$500 |

| 6-Month CD | 4.80% | 4.10% | $500–$1,000 |

| 1-Year CD | 4.65% | 4.25% | $500–$1,000 |

| 3-Year CD | 4.40% | 4.00% | $500–$1,000 |

| 5-Year CD | 4.25% | 3.85% | $500–$1,000 |

| Money Market | 4.90% | 4.15% | $1,000–$10,000 |

Source: FDIC National Rates and Rate Caps, March 2026; Bankrate survey of 100+ institutions

The 2026 Anomaly: Inverted Yield Curve

Typically, CDs pay more than savings accounts because you lock up your money. But in early 2026, HYSAs actually outpay CDs for terms under 2 years. Why?

-

Banks are flush with deposits and don’t need long-term commitments

-

Rate uncertainty makes banks hesitant to lock in 5-year payouts

-

Competition for liquid savings is fierce among online banks

What this means: For short-term savings (under 2 years), HYSAs currently win. For long-term security, CDs still have a role.

Part 2: High-Yield Savings Accounts—The 2026 Winners

Top 5 HYSAs (March 2026)

| Bank | APY | Minimum | Key Feature | FDIC Insured |

|---|---|---|---|---|

| UFB Direct | 5.15% | $0 | No fees, 24/7 support | Yes, $250k |

| Newtek Bank | 5.10% | $0 | Business accounts available | Yes, $250k |

| Bread Savings | 5.05% | $100 | Strong mobile app | Yes, $250k |

| Bask Bank | 5.00% | $0 | American Airlines miles option | Yes, $250k |

| Marcus (Goldman Sachs) | 4.90% | $0 | Same-day transfers, no fees | Yes, $250k |

Rates verified March 8, 2026. APYs are variable and subject to change.

How HYSAs Work in 2026

The Basics:

-

Online-only banks (no branches) offer higher rates by saving on overhead

-

Variable rates move with Fed policy—can rise or fall

-

Unlimited withdrawals (though some banks limit to 6/month per Regulation D)

-

Daily compounding interest for maximum growth

The Fine Print to Watch:

-

Introductory Rates: Some banks advertise “up to 5.50% APY”—but that’s only for the first 3-6 months. Check the ongoing rate.

-

Balance Tiers: “Earn 5.00% on balances up to $5,000, then 1.00% above.” For $20,000, your effective rate drops to 2.00%.

-

Activity Requirements: Some banks require monthly direct deposits or debit card transactions to earn the top rate.

-

Fees: Monthly maintenance fees, excess withdrawal fees, or inactivity fees can erase your interest.

Real-World Example: $25,000 Emergency Fund

| Account Type | APY | Annual Interest | 5-Year Total |

|---|---|---|---|

| Traditional Savings | 0.46% | $115 | $578 |

| Marcus HYSA | 4.90% | $1,225 | $6,765 |

| Difference | — | +$1,110/year | +$6,187 |

Assumes rates remain constant. Actual returns will vary.

Part 3: Certificates of Deposit—When Locking In Makes Sense

Top 5 CDs (March 2026)

| Bank | Term | APY | Minimum | Early Withdrawal Penalty |

|---|---|---|---|---|

| Ally Bank | 11 months | 4.85% | $0 | 60 days interest |

| Discover | 1 year | 4.70% | $2,500 | 6 months interest |

| Synchrony | 18 months | 4.60% | $0 | 180 days interest |

| Capital One | 3 years | 4.45% | $0 | 6 months interest |

| Barclays | 5 years | 4.30% | $0 | 180 days interest |

Rates verified March 8, 2026. CDs are fixed-rate products.

CD Strategies for 2026

Strategy 1: CD Laddering Instead of locking $30,000 in a 5-year CD, split it:

-

$6,000 in 1-year CD

-

$6,000 in 2-year CD

-

$6,000 in 3-year CD

-

$6,000 in 4-year CD

-

$6,000 in 5-year CD

Benefit: Every year, one CD matures. You reinvest at current rates (if rates rose) or keep cash (if you need it). Reduces interest rate risk.

Strategy 2: Barbell Approach

-

50% in HYSA (liquidity for emergencies)

-

50% in 2-3 year CDs (higher locked-in rates)

Benefit: Balances access with yield. In 2026’s inverted environment, this beats long-term CDs.

Strategy 3: No-Penalty CDs Banks like Ally and Marcus offer CDs you can break without fees. Rates are slightly lower (4.50% vs. 4.70%), but you keep flexibility.

When CDs Beat HYSAs in 2026

| Scenario | Winner | Why |

|---|---|---|

| Emergency fund (3-6 months expenses) | HYSA | Need instant access |

| Home down payment (buying in 1-2 years) | 1-year CD | Lock rate, preserve principal |

| College tuition (due in 3 years) | CD ladder | Predictable withdrawals |

| Retirement income supplement | 5-year CD | Guaranteed yield, low risk |

| “Sleep at night” money | CD | No rate fluctuation anxiety |

Part 4: Money Market Accounts—The Hybrid Option

Often overlooked, Money Market Accounts (MMAs) blend HYSA liquidity with checking features.

Top 2026 MMAs

| Bank | APY | Minimum | Checks? | Debit Card? |

|---|---|---|---|---|

| UFB Direct MMA | 4.90% | $5,000 | Yes | Yes |

| Capital One 360 MMA | 4.75% | $0 | Yes | Yes |

| Discover MMA | 4.65% | $2,500 | Yes | Yes |

Best for: Savers who need occasional check-writing (large purchases, quarterly tax payments) but want HYSA-level returns.

Trade-off: Usually higher minimum balances than HYSAs. Fall below minimum, and rates plummet or fees hit.

Part 5: The 2026 Tax Trap—Don’t Let Uncle Sam Eat Your Gains

Interest income is fully taxable at your ordinary income rate. In 2026:

| Tax Bracket | Federal Rate | State Rate (avg) | Total Tax on $1,000 Interest |

|---|---|---|---|

| 12% | 12% | 5% | $170 |

| 22% | 22% | 5% | $270 |

| 32% | 32% | 5% | $370 |

Solutions:

-

Series I Bonds: 5.27% composite rate (inflation-adjusted), federal tax-deferred, state tax-free. Limited to $10,000/year per person.

-

Municipal Money Market Funds: Tax-free at federal level (and state if buying home-state bonds). Current yield ~3.50% tax-free = ~5.20% taxable equivalent for high earners.

-

Roth IRA: Contribute $7,000/year (2026 limit). Growth and withdrawals tax-free in retirement. Not for emergency funds—early withdrawals penalized.

Part 6: Safety, FDIC Insurance, and Red Flags

FDIC Insurance Rules (2026)

-

Coverage limit: $250,000 per depositor, per institution, per ownership category

-

Joint accounts: $500,000 coverage ($250k per person)

-

Revocable trusts: $250,000 per unique beneficiary

Example: You can have $250k in a single account, $250k in a joint account with spouse, $250k in an IRA, and $250k in a trust account—all at the same bank, all fully insured ($1M total).

Warning Signs of a Sketchy Bank

❌ “Guaranteed 8% returns!” — Scam. No bank pays 8% in 2026.

❌ No FDIC logo or membership verification — Run.

❌ Requires wire transfer to open — Legitimate banks accept ACH.

❌ Customer service only via WhatsApp — Major red flag.

❌ Spelling errors on website — Professional banks proofread.

❌ No FDIC logo or membership verification — Run.

❌ Requires wire transfer to open — Legitimate banks accept ACH.

❌ Customer service only via WhatsApp — Major red flag.

❌ Spelling errors on website — Professional banks proofread.

Verify FDIC status: fdic.gov/bankfind

Part 7: The 7-Day Action Plan—Optimize Your Cash Today

Day 1: Audit Your Current Accounts

-

List all savings accounts

-

Note current APYs

-

Calculate monthly interest earned (spoiler: it’s probably depressing)

Day 2: Define Your Goals

| Goal | Timeline | Best Vehicle |

|---|---|---|

| Emergency fund | 0-6 months | HYSA |

| Vacation fund | 6-18 months | HYSA or No-Penalty CD |

| Down payment | 1-3 years | CD ladder |

| Wedding fund | 1-2 years | 1-year CD |

| Opportunity fund | Flexible | HYSA |

Day 3: Compare Rates

Use aggregator tools:

-

Bankrate.com

-

NerdWallet

-

DepositAccounts.com

Filter by: FDIC insured, no monthly fees, minimum deposit you can meet.

Day 4: Open Your Account

-

Online application takes 5-10 minutes

-

Have ready: SSN, driver’s license, current address, funding account info

-

Pro tip: Some banks offer new customer bonuses ($100-$300) for opening with $10k+

Day 5: Fund the Account

-

ACH transfer from existing bank (free, 1-3 days)

-

Wire transfer (same day, $15-$30 fee—only for large amounts)

-

Mobile check deposit (if funding from another account’s check)

Day 6: Set Up Automation

-

Schedule automatic monthly transfers from checking

-

Enable alerts for rate changes

-

Download mobile app for easy monitoring

Day 7: Close or Reduce Old Accounts

-

Leave $100 in old account to keep it open (helps credit score via account age)

-

Or close entirely if fees exist

-

Update any auto-payments linked to old account

Part 8: 2026 Rate Predictions—Lock In Now or Wait?

What the Experts Say

| Institution | 2026 HYSA Forecast | 2026 CD Forecast |

|---|---|---|

| Federal Reserve | 4.00%–4.50% by year-end | N/A |

| Goldman Sachs | 3.75%–4.25% | 3.50%–4.00% |

| Bank of America | 4.00%–4.75% | 3.75%–4.50% |

| Citi | 3.50%–4.25% | 3.25%–4.00% |

Consensus: Rates likely decline gradually through 2026 as the Fed eventually cuts. The current 5%+ HYSA rates are probably the peak for this cycle.

The Strategy

-

If you need liquidity: Open HYSA now. Rates may drop, but you’ll still beat inflation and traditional savings.

-

If you can lock money away: 1-2 year CDs at 4.60%+ preserve today’s rates before they fall.

-

If you’re rate-sensitive: CD ladder to hedge against both rising and falling rates.

Frequently Asked Questions (2026 Edition)

Q: Are online banks safe?

A: Yes—if FDIC insured. Online banks like Marcus, Ally, and Discover are as safe as Chase or Bank of America. The FDIC doesn’t care if the bank has branches. Your $250k coverage is identical.

Q: Can I lose money in a HYSA or CD?

A: No, with two caveats: (1) Inflation can erode purchasing power even as dollar balance grows, and (2) Early CD withdrawal penalties can eat into principal if you break the term.

Q: How often do HYSA rates change?

A: Variable rates can change anytime, but typically move with Fed policy. In 2022-2023, top HYSAs adjusted monthly. In 2024-2025, changes slowed to quarterly. Expect 2-4 rate adjustments in 2026.

Q: What’s the catch with 5%+ rates?

A: No catch—just economics. Online banks save on branch costs and pass savings to you. The “catch” is that rates are variable and will likely decline. Enjoy them while they last.

Q: Should I put my emergency fund in a CD?

A: No. Emergencies don’t wait for CD maturity dates. Use HYSA for emergency funds. The slightly lower rate is worth the instant access.

Q: Do I pay taxes on HYSA/CD interest?

A: Yes. Banks issue 1099-INT for accounts earning $10+ in annual interest. Report on your tax return. State taxes apply too, unless using municipal products.

Q: What happens if my bank fails?

A: FDIC takes over (usually Friday evening). By Monday, your account is transferred to a healthy bank or you’re mailed a check for insured balance. No depositor has lost insured funds since FDIC creation in 1933.

Conclusion: The $800 Decision

You have three options for your cash in 2026:

Option A: Do Nothing

Keep money in traditional savings at 0.46%. Earn $46/year on $10,000. Fall behind inflation.

Keep money in traditional savings at 0.46%. Earn $46/year on $10,000. Fall behind inflation.

Option B: Optimize with HYSA

Move to 5.00% HYSA. Earn $500/year. Gain $454 in annual passive income. Keep full liquidity.

Move to 5.00% HYSA. Earn $500/year. Gain $454 in annual passive income. Keep full liquidity.

Option C: Lock with CDs

Build CD ladder at 4.60% average. Earn $460/year. Guarantee returns even if rates drop.

Build CD ladder at 4.60% average. Earn $460/year. Guarantee returns even if rates drop.

The difference between Option A and B/C? $4,000–$4,500 over 10 years—on just $10,000. Scale that to $50,000 or $100,000, and we’re talking life-changing money for 30 minutes of work.

High-yield savings and CDs aren’t exciting. They won’t make you rich overnight. But in 2026’s uncertain economy, guaranteed 4-5% returns with zero risk is a wealth-building superpower most people ignore.

Don’t be most people. Move your money today.

Ready to Earn 5% on Your Savings?

[Compare Top High-Yield Savings Accounts →]

See today’s best rates from FDIC-insured banks. Open online in minutes.

[Explore CD Rates and Ladder Options →]

Lock in guaranteed returns before rates drop.

Sources & Methodology

-

FDIC National Rates and Rate Caps, March 2026

-

Federal Reserve Economic Data (FRED), St. Louis Fed

-

Bankrate National Survey of 100+ financial institutions, March 2026

-

NerdWallet HYSA and CD rate tracking

-

DepositAccounts.com rate aggregation

Rates verified as of March 8, 2026. APYs are annual percentage yields and assume compounding. Minimum deposits and terms subject to change. Verify current rates directly with institutions before opening accounts.

Advertiser Disclosure

This site is an independent, advertising-supported comparison service. We may receive compensation when you click on links to products or services from our advertising partners. This compensation may impact how and where products appear on this site, including the order in which they appear.

We strive to provide accurate, up-to-date information; however, all rates, terms, and conditions are subject to change without notice. We do not include all companies or all available products. Our goal is to help you make informed financial decisions, not to steer you toward specific providers.

Editorial integrity: Our writers and editors are not influenced by our advertising relationships. Opinions expressed are solely those of the author.

About This Site

globespro4g.com is a personal finance education platform. We are not a bank, lender, or investment advisor. Content is for informational purposes only and should not be construed as financial advice. Consult a qualified financial professional before making significant financial decisions.

FDIC insurance: $250,000 per depositor, per insured bank, for each account ownership category. Visit fdic.gov for details.

Leave a Reply