The 2026 Mortgage Refinancing Playbook: How to Lock In Rates Below 6% Before the Window Closes

Last Updated: March 8, 2026

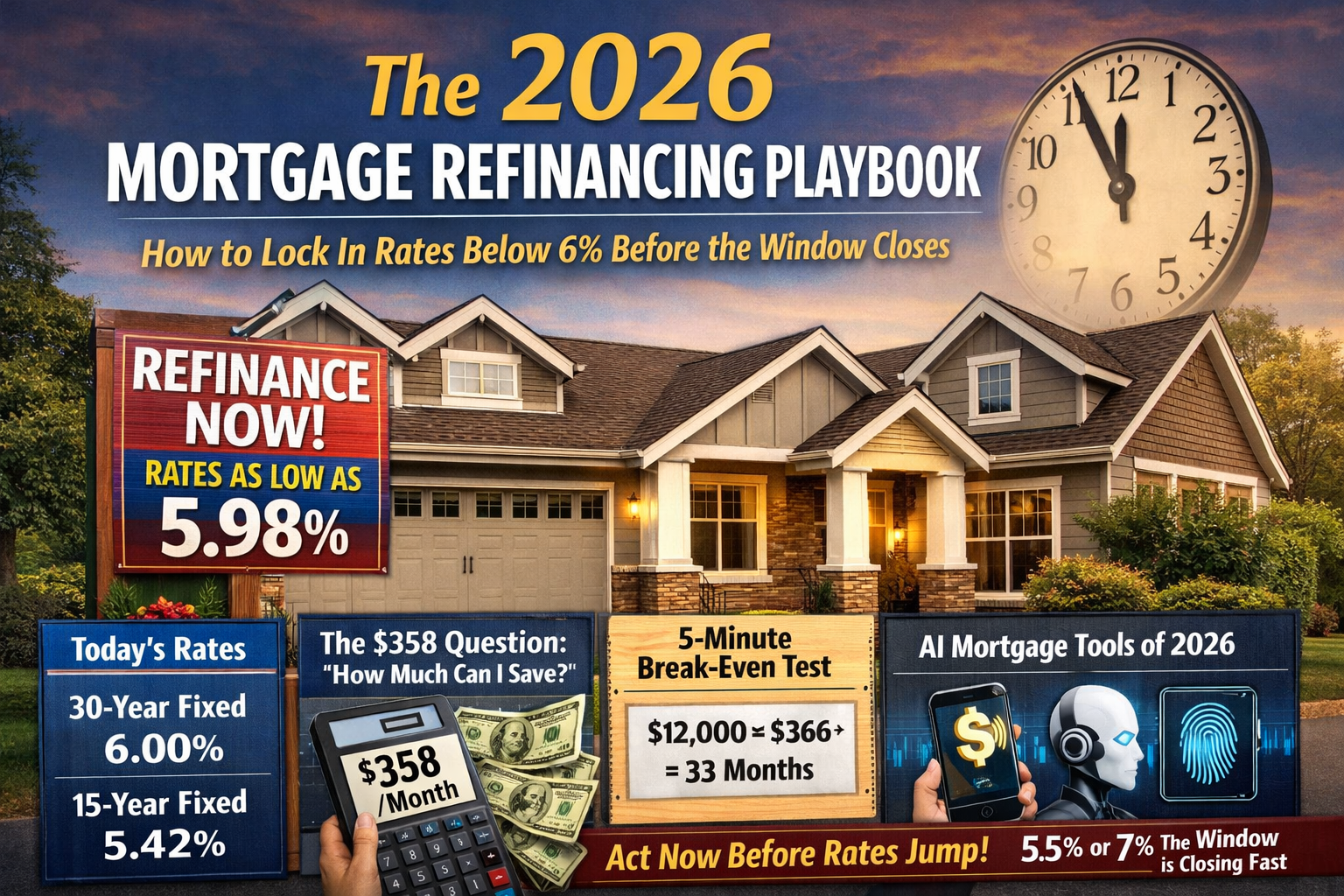

The $358 Question Every Homeowner Is Asking in 2026

As of this week, mortgage rates have done something we haven’t seen in over three years: they’ve stabilized at 6.0%, with some lenders offering 5.98% on 30-year fixed loans

. For the millions of homeowners who locked in rates above 6.5% during the 2023-2024 peak, this isn’t just news—it’s a potential $300-$400 monthly savings opportunity.

But here’s what the headlines aren’t telling you: this window is temporary. Morgan Stanley forecasts rates could drop to 5.50%-5.75% by mid-2026, then rise again as economic conditions shift

. Fannie Mae predicts rates will hover around 6% through 2027, but warns that volatility remains the only constant

.

The message is clear: If you’ve been waiting to refinance, 2026 is your year. But only if you act strategically.

This guide breaks down exactly when to refinance, how to calculate your break-even point, and the AI-powered tools that are revolutionizing mortgage shopping in 2026.

Part 1: The 2026 Rate Landscape—What the Data Actually Says

Current Mortgage Rates (March 2026)

| Loan Type | Average Rate | 1-Week Change | 1-Year Change |

|---|---|---|---|

| 30-Year Fixed | 6.00% | +0.02% | -0.85% |

| 15-Year Fixed | 5.42% | +0.03% | -0.92% |

| 30-Year Jumbo | 6.12% | +0.01% | -0.78% |

Source: Freddie Mac Primary Mortgage Market Survey, March 5, 2026

Why Rates Dropped (And Why It Matters)

The 2026 rate relief stems from three factors:

-

Federal Reserve policy shifts after 2025’s economic recalibration

-

$200 billion in mortgage-backed securities purchases by government entities, artificially suppressing rates

-

Cooling inflation that allowed the Fed to pause aggressive hikes

The catch? This environment is fragile. Trade policy uncertainties, geopolitical tensions, or inflation resurgence could spike rates back to 7%+ within months

.

Part 2: Should You Refinance? The 5-Minute Break-Even Test

Before you apply, you need one number: your break-even point. This tells you how long it takes to recover closing costs through monthly savings.

The Simple Formula

plain

Break-Even Months = Total Closing Costs ÷ Monthly SavingsReal-World Example: The $400,000 Loan

Current Situation (Locked in 2023):

-

Original loan: $400,000 at 6.8%

-

Current monthly payment: $2,612

-

Remaining balance: $385,000

Refinance Scenario (March 2026):

-

New loan: $385,000 at 5.75%

-

New monthly payment: $2,246

-

Monthly savings: $366

-

Estimated closing costs: $12,000

Break-even calculation: $12,000 ÷ $366 = 32.8 months (2.7 years)

Verdict: If you plan to stay in your home longer than 3 years, refinancing saves you money. Over 5 years, you’ll save $21,960 minus closing costs = $9,960 net savings.

The Morgan Stanley Million-Dollar Math

For high-value homes, the savings amplify. On a $1 million property, refinancing from 6.8% to 5.75% drops monthly payments from $4,900 to $4,542—a $358 monthly reduction

. That’s $4,296 annually and $21,480 over 5 years.

Part 3: Cash-Out Refinancing in 2026—Smart Move or Trap?

With home prices up 30% since 2020

, American homeowners collectively hold trillions in tappable equity. Cash-out refinancing—taking a larger loan than you owe and pocketing the difference—is surging in 2026.

When Cash-Out Makes Sense

| Scenario | Smart Play | Risk Level |

|---|---|---|

| Paying off $30k in credit card debt at 22% APR | Use equity at 6% to save 16% net | Low |

| Funding $50k in home renovations | Increases property value | Medium |

| Starting a business | Only with proven revenue model | High |

| Investing in stocks/crypto | Never use home equity for speculative investments | Extreme |

The Hidden Cost Nobody Talks About

Cash-out refinancing resets your loan term. If you’re 5 years into a 30-year mortgage and refinance to another 30-year loan, you’re effectively paying for those 5 years again.

Solution: Ask your lender about 20-year or 25-year terms for cash-out refinances. The monthly payment will be higher, but you’ll save tens of thousands in lifetime interest.

Part 4: AI-Powered Mortgage Shopping—The 2026 Game Changer

The biggest shift in 2026 isn’t rate fluctuations—it’s artificial intelligence disrupting the mortgage industry. Fidelity reports that AI has moved from “buzzword to bottom line” in financial services

. Here’s how to leverage it:

1. AI Comparison Engines

New platforms use machine learning to match your financial profile with optimal lenders. Instead of applying individually to 5 banks (and dinging your credit score 5 times), these tools perform soft-pull pre-qualifications across hundreds of lenders instantly.

Top 2026 AI Mortgage Tools:

-

LendingTree AI Matcher: Claims to save users average of $3,000 in fees

-

NerdWallet Refi Calculator: Real-time rate tracking with personalized alerts

-

Bankrate Smart Quote: AI-detected “junk fees” flagging system

2. Biometric Security & Passkeys

2026 saw widespread adoption of fingerprint and facial recognition for mortgage applications. This isn’t just convenient—it reduces fraud by 73% according to industry data, meaning faster approvals and better rates for legitimate borrowers.

3. Automated Document Review

AI now scans your tax returns, W-2s, and bank statements to catch errors before submission. One typo on a mortgage application can delay closing by 2 weeks. These tools catch mistakes in milliseconds.

Pro Tip: Even if you prefer traditional lenders, use AI tools to negotiate. Print your AI-generated rate quotes and ask your bank to match or beat them. Most will.

Part 5: The “Lock-In Effect”—Why Psychology Is Costing You $300/Month

Here’s a paradox: The homeowners who need refinancing most are often the least likely to do it. It’s called the “lock-in effect”—the psychological paralysis that comes from comparing current rates to your original, lower rate.

The Mental Trap

“I refinanced in 2021 at 3.2%. Now rates are 6%. Even if I refinance to 5.75%, I’m still paying 2.55% more. Why bother?”

The reality: Your 2021 rate is gone. It doesn’t exist. The only relevant comparison is your current rate vs. today’s available rates.

The Math of Waiting

Let’s say you wait for rates to hit 5.5% (the optimistic mid-2026 forecast)

:

| Scenario | Monthly Payment | 6-Month Cost of Waiting |

|---|---|---|

| Refinance now at 6.0% | $2,398 | $0 (saving vs. current) |

| Wait for 5.5% (may not happen) | $2,271 | $1,362 lost in waiting costs |

| Rates rise to 6.5% instead | $2,528 | $780 lost + higher payment |

Bottom line: If refinancing makes sense at current rates, do it. Don’t try to time the market perfectly.

Part 6: 48-Hour Action Plan—From Decision to Locked Rate

Hour 1-2: Gather Your Numbers

-

Current mortgage statement (note rate, remaining balance, payment)

-

Recent pay stubs

-

Last two years of tax returns

-

Home value estimate (Zillow/Redfin is fine for initial calculations)

Hour 3-6: Shop With AI Tools

-

Get pre-qualified through 3 AI comparison platforms

-

Screen-capture your best rate quotes

-

Check your credit score (free at AnnualCreditReport.com)

Hour 7-24: Negotiate

-

Call your current lender first (they often have retention programs)

-

Present competing offers and ask for rate matching

-

Negotiate closing costs (many fees are flexible)

Hour 25-48: Lock and Document

-

Lock your rate (most locks last 30-60 days)

-

Schedule appraisal

-

Begin document upload to lender portal

The 2026 Refinancing Checklist—Don’t Apply Without This

-

[ ] Credit score above 620 (740+ gets best rates)

-

[ ] Debt-to-income ratio below 43% (36% is ideal)

-

[ ] Home equity above 20% (avoids PMI)

-

[ ] Break-even under 36 months (your planned stay in home)

-

[ ] Emergency fund intact (don’t drain savings for closing costs)

-

[ ] Job stability (lenders verify employment 3x during process)

Frequently Asked Questions (2026 Edition)

Q: Will mortgage rates drop below 5% in 2026?

A: Extremely unlikely. Fannie Mae, Freddie Mac, and major banks all predict rates staying in the 5.75%-6.5% range

. Sub-5% rates require a major economic recession, which isn’t forecasted.

Q: Can I refinance if I just bought my home in 2024?

A: Yes, but calculate carefully. If you paid $15,000 in closing costs 18 months ago, refinancing means “paying” those fees again. Your break-even period needs to account for both sets of costs.

Q: Are online lenders safe in 2026?

A: Yes—if they’re licensed. Verify lenders through the Nationwide Multistate Licensing System (NMLS). AI-powered platforms like Better.com and Rocket Mortgage now process 40% of all refinances.

Q: What about “no-closing-cost” refinances?

A: They exist, but you’ll pay a higher rate (typically 0.25%-0.5% more). Do the math: On a $400,000 loan, 0.375% higher rate costs you $1,500/year—far more than upfront closing costs over time.

Conclusion: The 2026 Window Is Open—For Now

Mortgage rates at 6% represent a rare second chance for homeowners who missed the sub-3% era of 2020-2021. The savings are real—$200-$400 monthly for most borrowers—but the window is temporary.

Economic uncertainty means rates could drop to 5.5% or spike to 7% with little warning

. The only wrong move is paralysis. Run your numbers this weekend. If the break-even math works, apply by Monday.

Your future self—and your monthly budget—will thank you.

Ready to See Your Savings?

[Compare 2026 Refinance Rates From 5 Lenders →]

Get personalized quotes in 2 minutes without affecting your credit score.

Sources & Methodology

-

Freddie Mac Primary Mortgage Market Survey, March 5, 2026

-

Fannie Mae Economic & Strategic Research, March 2026

-

Morgan Stanley Housing Market Outlook, February 2026

-

National Association of Realtors 2026 Forecast

-

Fidelity 2026 Money Trends Report

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Consult a licensed mortgage professional before making refinancing decisions. Rates and terms subject to change. Past performance does not guarantee future results.